Tax Clarity Newsletter

October 1, 2025

💌 Today’s Thing: Some Changes About How You Will Be Able Manage Your Retirement Money

Some current matters about your money. Stuff needing some Tax Clarity – – –

If you’re at an age where the idea of retirement is no longer your distant pipedream, you should know that the options to use a portion of your income before the federal government takes its tax bite are about to become narrower. Two weeks ago, a new Treasury regulation1 mandated that catch-up contributions that allow greater contribution amounts for those age 50 and above will have to be from after-tax income if their FICA wages (indexed for inflation) from the same employer are greater than $145,000. This final regulation implements a statutory change by the SECURE 2.0 Act of 20222.

Just like I said last week, the language of this one is a bit convoluted. But this is what we’re here for. Let’s get into it…

🧾 The deets…clean and quick

The bottom line is…after this year, many individual investors won’t be able use as much pre-tax income to fund their retirement savings plans as before.

A bit of background: for those in the workforce who need a reminder, the days of handsome pensions with defined benefits faded into memory long ago. Defined contribution plans, such as 401(k) plans (named after the applicable section of the Federal tax code) became the vehicle for people to invest in their own retirement without ties to one specific employer. These are retirement savings plans where the amount contributed is defined, but the future benefits can vary based on investment performance.

🧾 WHY does this matter to you?

For individuals around age 50, these plans work in the following way:

Contributions: Individuals contribute a portion of their salary to the plan, often with pre-tax dollars. Employers may also match a portion of these contributions, which can significantly boost retirement savings.

Investment Choices: The contributions are invested in a selection of funds chosen by the individual or the employer’s contractor. These can include stocks, bonds, and other investment options. The performance of these investments will determine the growth of the retirement savings.

Tax Advantages: Contributions are typically made with pre-tax dollars, reducing taxable income. The investments grow tax-deferred, meaning taxes are not paid on the earnings until the money is withdrawn.

Catch-Up Contributions: Individuals age 50 and over have an option to make additional “catch-up” contributions. This allows them to contribute more than the standard annual limit, helping to increase the contribution to their savings as they approach retirement.

Withdrawals: Upon reaching retirement age, individuals can start withdrawing from their plan. The withdrawals are taxed as ordinary income, that is, at the individual’s marginal tax rate. It’s important to note that early withdrawals (before age 59½) may incur penalties and taxes.

Required Minimum Distributions (RMDs): Starting at age 73, individuals must begin taking RMDs (withdrawals) from their plan. The amount is based on life expectancy and the account balance.

💵 WHAT is this “catch-up” thing about?

“Catch-up eligible participants” as defined by Treas. Reg. 1.414(v)-1(g)(3) are allowed to contribute an additional $7,500 per year above the 2025 statutory limit of $23,500 for 401(k) plans, which are traditional 401(k)s for pre-tax income, Roth 401(k)s for after-tax income, or a combination of the two. For 2025, the SECURE 2.0 Act of 2022 increases the applicable dollar catch-up limit under IRC §414(v)(2)(B)(i) and (ii) in the case of a catch-up eligible participant who reaches age 60, 61, 62, or 63 during the taxable year. They are allowed to contribute up to an additional $11,250 of their pre-tax income. However, the new regulation will require the additional catch-up amounts to be contributed to a Roth 401(k) from after-tax income.

📅 WHEN do the changes kick in?

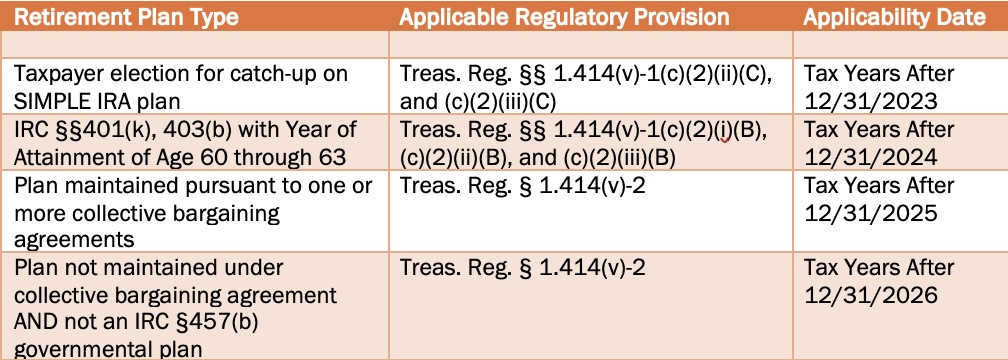

The effect of the new regulation on tax planning for current retirees, employers, and current and future retirement plan participants is significant. While the rule takes effect on November 17, 2025, it will be generally applicable to tax years beginning after December 31, 2026. However, other tax years may be affected depending on taxpayer elections under related retirement plan types such as SIMPLE IRA plans, §403(b), and §457(b).

When Does It Start?

This regulation doesn’t make any revisions to the regulations relating to eligible governmental 457(b) plans (those for deferred compensation plans of State and local governments and tax-exempt organizations) because those regulations do not currently provide for the inclusion of a qualified Roth contribution program in an eligible governmental 457(b) plan3.

One way or another, this regulation affects anyone who has worked at a company where they have participated in one of its retirement plan offerings. Individual employees and the employer companies and other institutions will have to find their way toward compliance in this evolving tax environment.

There’s the scoop, everyone! Thanks for taking time to check out the inaugural Tax Clarity Newsletter. If you want to join our mailing list, subscribe and receive a direct copy every Wednesday, or provide any feedback, send an e-mail to admin@sweetclarity.com.

Thank you so much!

References (3)

1 Department of the Treasury, Catch-Up Contributions, 90 Fed. Reg. 44527 (September 16, 2025), https://www.federalregister.gov/documents/2025/09/16/2025-17865/catch-up-contributions

2 Pub. L. 117-328, 136 Stat. 4459 (2022), SECURE 2.0 Act, §603.

3 Catch-Up Contributions, 90 Fed. Reg. 44527, at 44544.

DISCLAIMER: The information in this newsletter is derived from public information, provided for education purposes. It is not provided as a financial advisory service and should be relied upon as such. For advice on a specific tax matter, please consult a tax professional.

© 2025 Sweet Clarity Media, LLC. All rights reserved.